Job loss, injuries, divorce, sudden illnesses — there are numerous events in life that can lead to the accumulation of large amounts of debt. If you find yourself facing an unmanageable debt load, bankruptcy may be the right tool to use to get things back on track. A Chapter 13 bankruptcy lawyer can help you hit that reset button on life.

At ARM Lawyers, our attorneys are passionate about helping people regain control of their financial lives. With more than 100 years of combined experience, we understand the complexities of bankruptcy and we are here to guide you through the process and into a brighter future. We often do that using Chapter 13 bankruptcy and debt restructuring.

Should I consider Chapter 13?

Chapter 13 is designed to set you up with one manageable, interest-free monthly payment. The payment amount is based on your ability to pay. Therefore, you will need to have some steady income in order to utilize this option. As a general rule, our Chapter 13 bankruptcy lawyers encourage clients to think of this as an option if:

- The person has a source of stable income

- Their income is too high to qualify for Chapter 7 debt liquidation

- They own non-exempt assets that could be sold by a Chapter 7 trustee

- The person is facing overwhelming credit card debt, medical bills or are behind on mortgage payments.

- They have received a bankruptcy discharge within the previous eight years.

When you file for Chapter 13, your debts will be reorganized by the court. You will receive a three- to- five- year repayment plan. The amount of the payments are generally proportional to your ability to pay. Your payments will first be applied to secured debt (such as your mortgage). At the end of the plan, you will be considered current on those secured loans, and any unsecured debt (like credit card debt) that remains will be eliminated. Thus, despite the fact that you are making payments, you may not pay anything to unsecured creditors.

Like Chapter 7, Chapter 13 puts a stop to creditor harassment, home foreclosure, and wage garnishment. Moreover, you retain complete control over your assets, making it preferred to Chapter 7 in cases in which you have non-exempt assets.

One thing that can be helpful is to estimate your Chapter 13 monthly plan payment and compare that to your current monthly obligations, which you can do below using a Chapter 13 calculator.

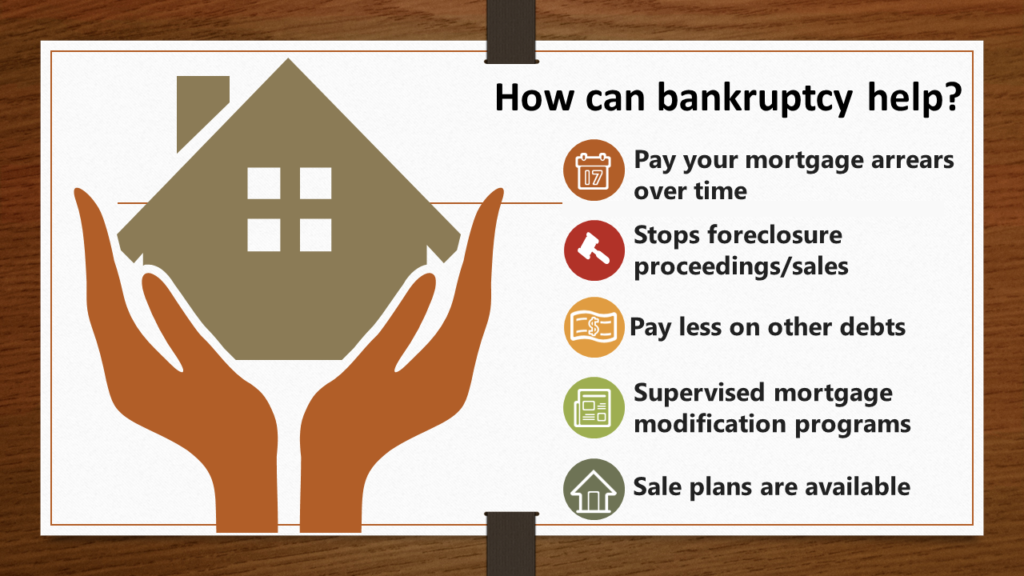

I’m behind on my mortgage. Can bankruptcy help?

Yes! Chapter 13 bankruptcy can stop a foreclosure sale or tax sale just by filing a bankruptcy petition. We can then use the Chapter 13 Plan to repay your mortgage arrears over time. You can even request a mortgage modification to try to lower your mortgage payments if you qualify. As a result, Chapter 13 bankruptcy provides a number of powerful options if you are late on your mortgage and like to keep your home.

Using a Chapter 13 bankruptcy to stop foreclosure is common, but we still get questions on this frequently. So much so that we decided to discuss it on “Bankruptcy Basics”. If you’d like to know more about using a Chapter 13 to save your house, you should watch this video:

Can bankruptcy lower my car payment?

Yes! In a Chapter 13 bankruptcy we have a lot of control over your secured debts including car payments. In many cases we can “cram down” your car loan so that you only pay the current value of the vehicle. This is great because cars depreciate. If you have owned your car for more than 910 days (2 and a half years), you may be entitled to lower the principal balance.

Don’t worry though, even if you don’t qualify for a cram down, we can usually reduce your interest rate and monthly payment anyway. We would simply elect to pay your car payment through your Chapter 13 Plan!

Chapter 13 bankruptcy is a powerful financial tool that can help you get back on track.

Chapter 13 bankruptcy process

What happens after I file a Chapter 13 bankruptcy? From the time you file the bankruptcy petition, you will be protected by the “automatic stay”. This protects you from collection activity of any kind unless and until the creditor gets permission from the court to proceed. Normally, at the time you file your petition, you would include your Chapter 13 Plan which sets forth your payment schedule. If you are working with a Chapter 13 bankruptcy lawyer, he or she would prepare this plan for you. The exact form of the plan varies from state to state and from District Court to District Court.

About four to six (4 to 6) weeks later, you will have your 341 Meeting of Creditors which is an opportunity for you to meet the Chapter 13 Trustee. Shortly thereafter, you will have a “confirmation hearing” in which the Bankruptcy Judge will review your Chapter 13 Plan to see if it meets the requirements of the Bankruptcy Code. Sometimes, your Chapter 13 bankruptcy lawyer will have to make revisions. That’s ok though, it happens frequently.

After your Chapter 13 Plan is confirmed, you’ll simply need to complete your Debtor Education Course and complete your plan payments.

If you’d like to know more about what happens after you file a Chapter 13 bankruptcy, we have a more detailed analysis here.